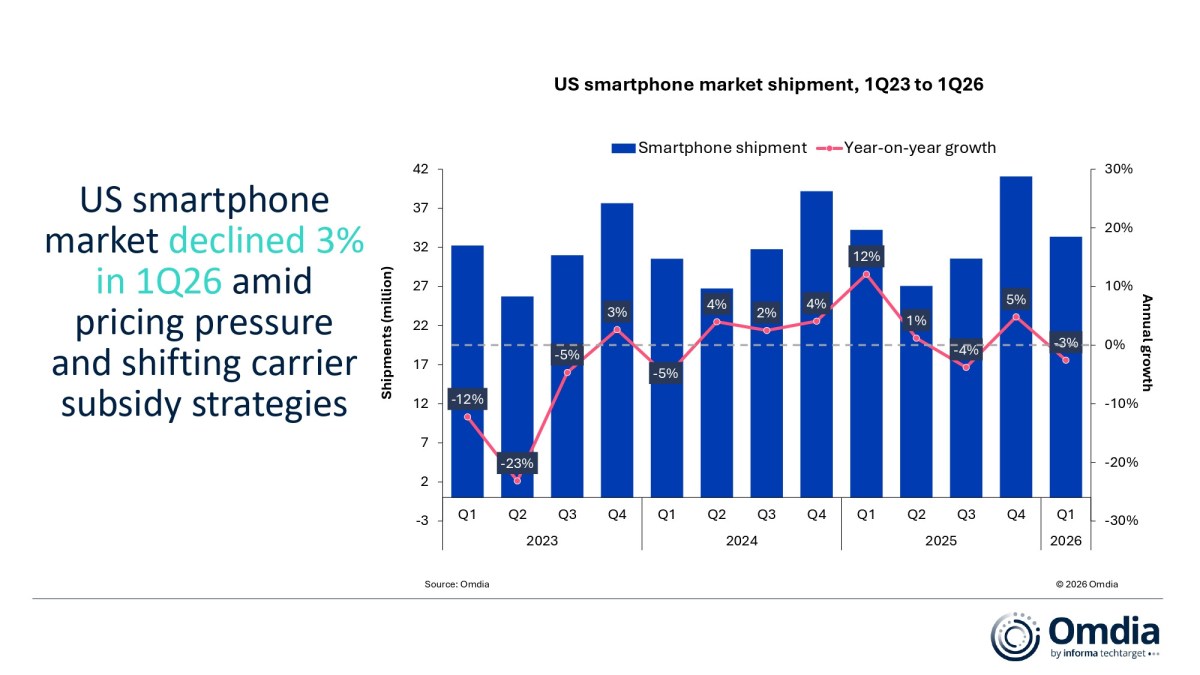

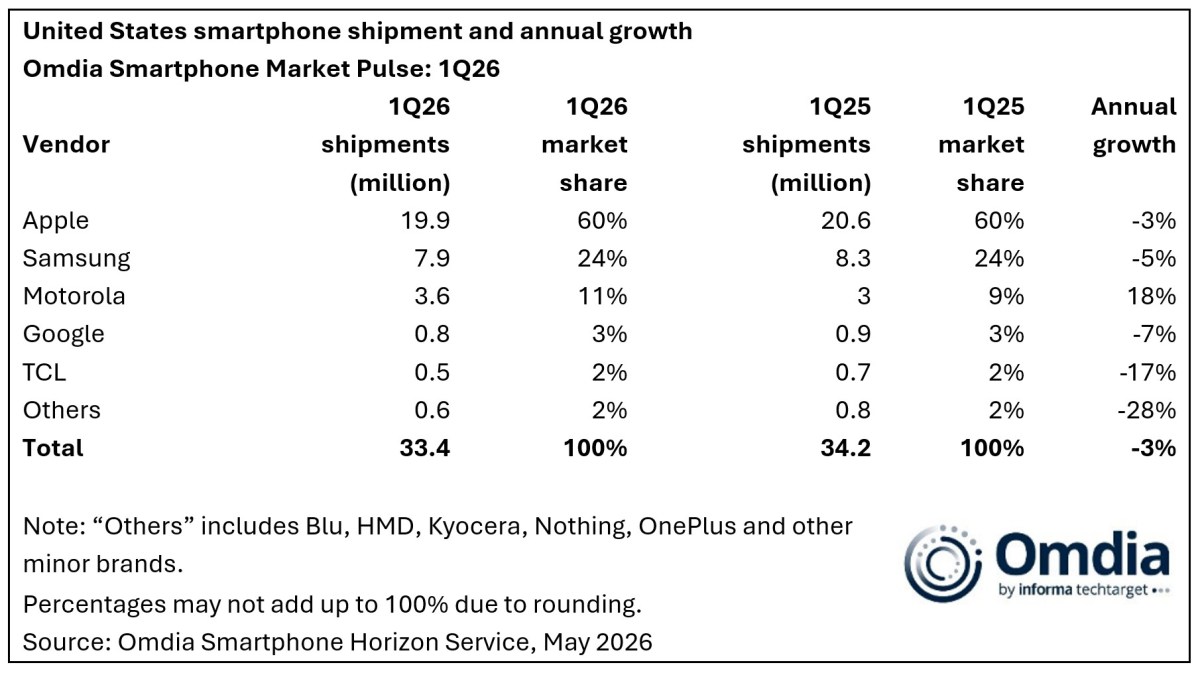

Omdiya has just shared its analysis on the US smartphone market in the first quarter of 2026 and things are not looking too good. The overall market declined 3% year-on-year to 33.4 million units.

First, the decline in Q1 2026 comes after smartphone makers accelerated inventory build-up in Q1 2025 in anticipation of upcoming import tariffs imposed by the Trump administration. Secondly, the smartphone market is beginning to feel the pressure of ever-increasing prices of memory chips and there has been a significant slowdown in smartphone purchases.

Additionally, delayed smartphone launches contributed to more compressed sales in Q1. Take the Galaxy S26 series, for example, which arrived about a month later than 2025.

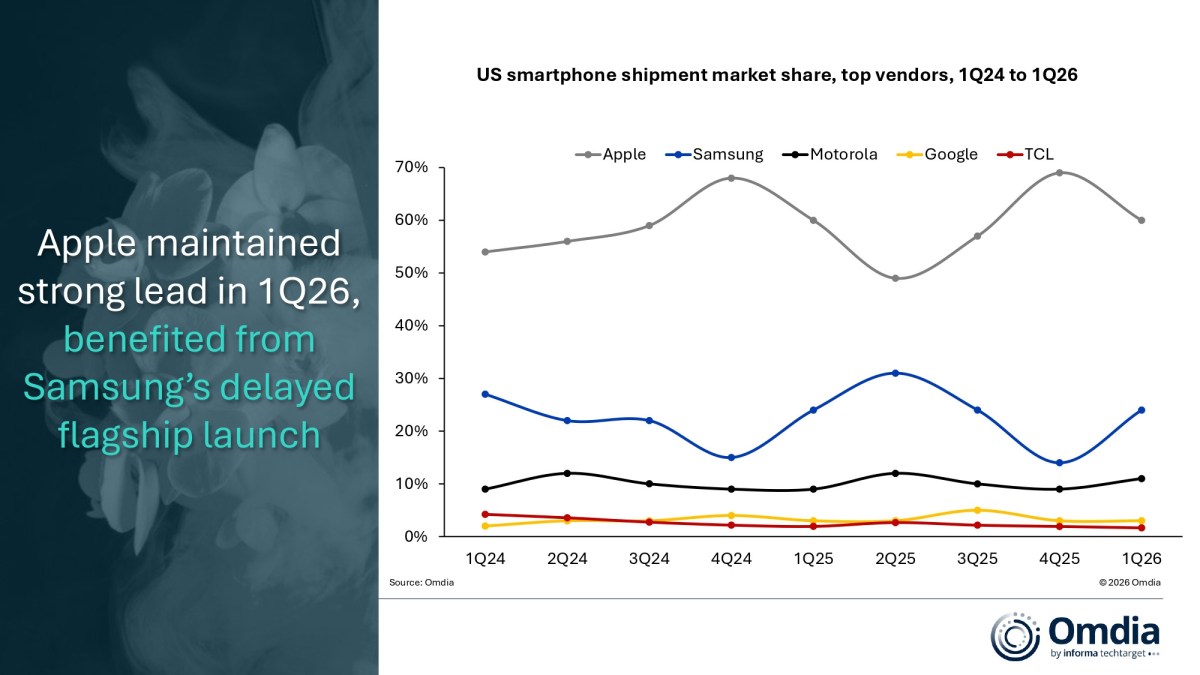

Talking about Samsung, the latter launch helped Apple secure more shipments in the premium segment as consumers decided to onboard the iPhone 17 instead. This series accounted for 70% of all Apple shipments. And even though Apple retained its leading position, its shipments declined 3% year over year.

Naturally, Samsung is in second place, but it has declined by 5% compared to the same period last year. The late launch of the Galaxy S26 was partly to blame for this, despite a relatively strong performance. The Galaxy S26 series saw a 25% increase in pre-orders compared to the Galaxy S25 lineup.

Motorola was the only smartphone OEM to show growth. The company achieved 18% more shipments compared to Q1 2025, largely thanks to its updated Moto G portfolio, which accounted for more than 70% of all Motorola shipments.

Google reported a 7% decline as sales of the Pixel 10 series remained flat, and the initial Pixel 10a launch was not enough to offset the underperforming Pixel 10 series.

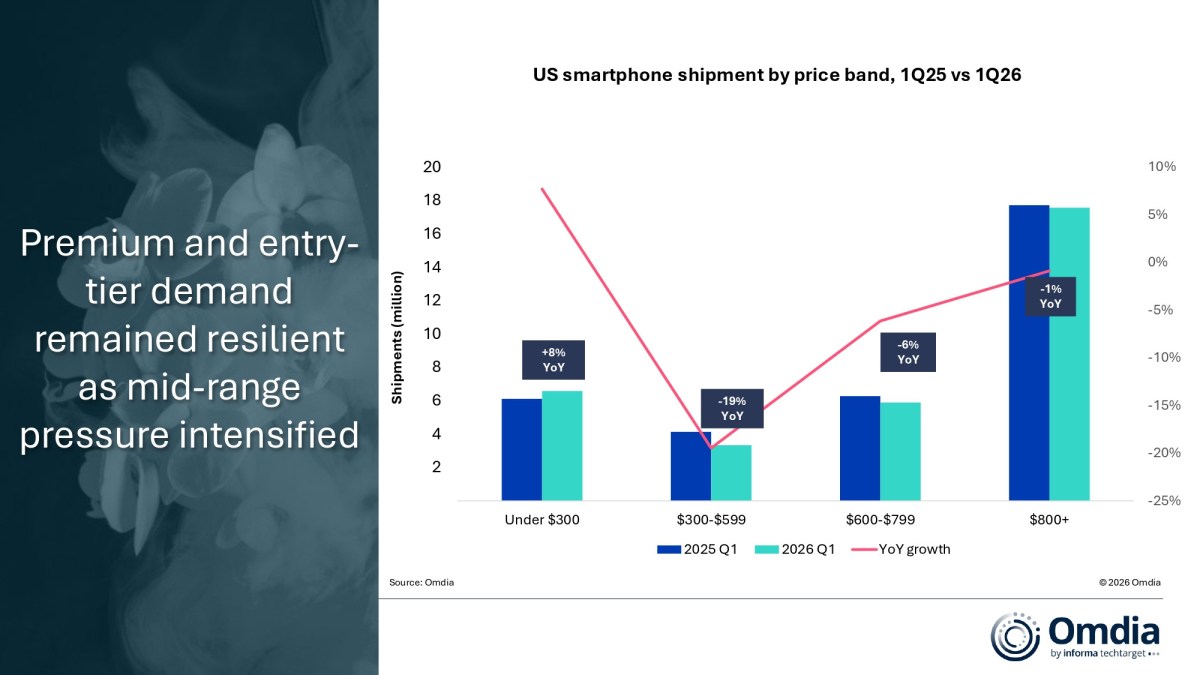

Another important finding from the analysis is that the US market is becoming more polarized over time. The premium and low-end segments appear to be more resistant to current market conditions than the mid-range tier. The sub-$300 category grew 8% while the premium $800+ category declined only 1%. The $300-599 and $600-700 ranges fell 19% and 6%, respectively.

Omdia believes that stronger collaboration with local carriers and plan-linked promotions are the way forward, as they will mitigate the impact of rising component costs on consumers. Analysts estimate a 4% market contraction for the entire year 2026.