Buying a house or property with cryptocurrency? The new American plan may soon make it possible

A new American instructions may soon allow homebupers to use cryptocurrency as evidence of property for mortgage applications, indicating increasing acceptance of digital funds in traditional finance.

Listen to the story

In short

- US government soon to accept cryptocurrency as asset

- Borrowers will not need to sell crypto to qualify for hostage

- Only property count on US-wheeled exchanges

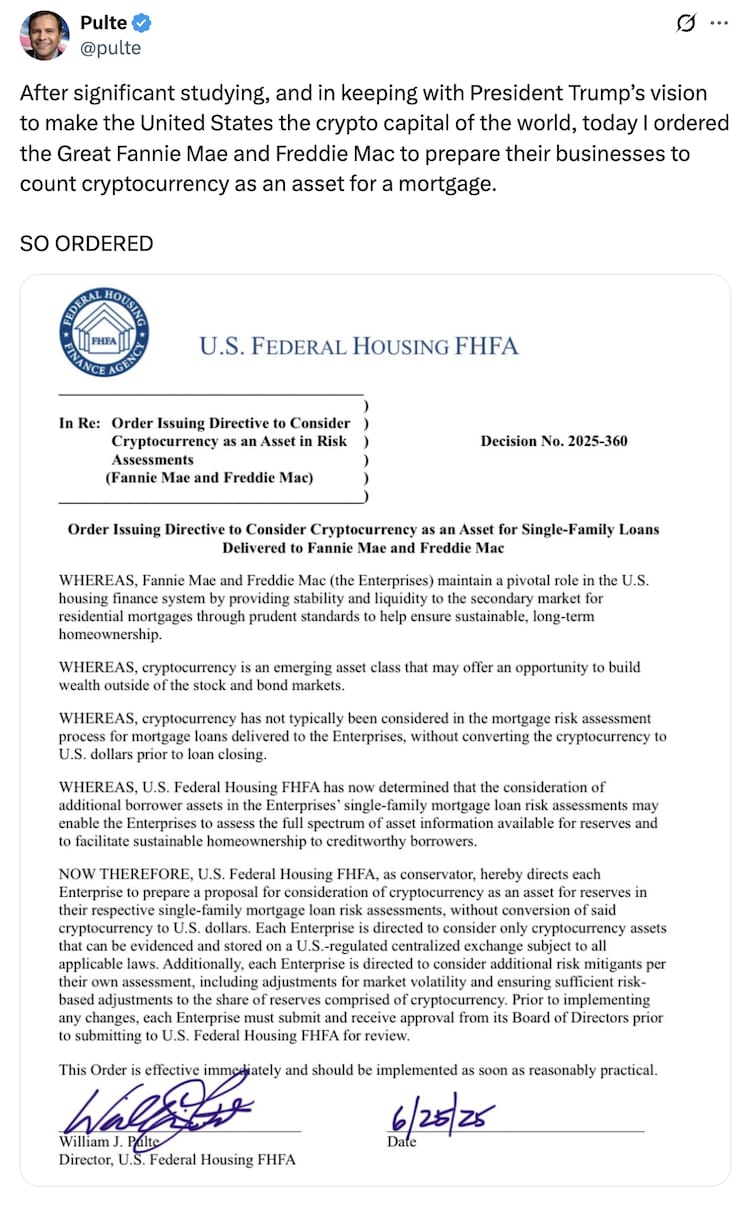

According to a CNN business report, the US government has directed the US government to prepare a plan to accept cryptocurrency as a property. William “Bill” Pulte, who oversees the Federal Housing Finance Agency (FHFA), announced the decision in a social media post on Wednesday. “After important studies, and keeping in mind the vision of President Trump, to make the United States the world’s crypto capital, today I ordered the great Fanny Mae and Freddy Mac to prepare their businesses to count the cryptocurrency as a property for a hostage,” he wrote.

It marks a rapid policy change in the real estate market in the US. Until now, homebuits could not include cryptocurrency in their financial profiles until they did not sell it and transferred money to traditional bank account. Under the previous guidance issued during the Biden administration, Crypto was considered very unstable to include the hostage calculation.

The new plan, however, recognizes Crypto as an emerging property class. As per the instructions, borrowers will no longer need to liquid their digital assets to qualify for home loans. Instead, they can list the stock or bond as well as eligible crypto holdings in their application-provided that those holdings are placed on US-regulated, centralized exchanges.

This distinction is important. According to FHFA instructions, crypto assets stored in private wallets or offshore exchanges will not be qualified.

Change is a possible game-changer for self-employed individuals or irregular income. In traditional loans, borrowers often require stable cash reserves. For crypto holders with traditional savings deficiency, their digital property can now serve as a buffer required to be approved.

Nevertheless, this step does not come without caution. Pulte allegedly directed both Fanny Maai and Freddy Mac to consider the risk-clan strategies. This means that the lenders will probably apply adequate discounts at the declared price of crypto holdings and require additional documentation – such as exchanges and evidence of stability over time.

The process will take some time to roll out completely. Fanny and Freddy must first prepare the proposals, approve them by their boards, and submit them to FHFA for final review. The new crypto mortgage guidelines will be implemented only after these stages.

Palte’s instruction also comes amidst the comprehensive plans to return Fanny and Freddy to personal ownership after 17 years of federal control. The plan indicated by President Donald Trump has expressed concern among some experts who worry that it may increase the cost of borrowing without the government’s security trap. Nevertheless, Crypto’s inclusion in the hostage idea shows how soon the digital finance is entering the mainstream. The instruction itself describes the cryptocurrency “as an emerging property class that can provide an opportunity to create money outside the stock and bond markets.”