“We model the model of 21%/17%/21%income/EBITDA/PAT CAGR on FY26–28E. We repeat our by -rating with the TP of INR 700,” Motilal Oswal added that he has maintained its EPS estimates for FY26 and FY27.

-

Productivity

Micros .Futs to Zero to Hero: Full Excel Guide

-

Money

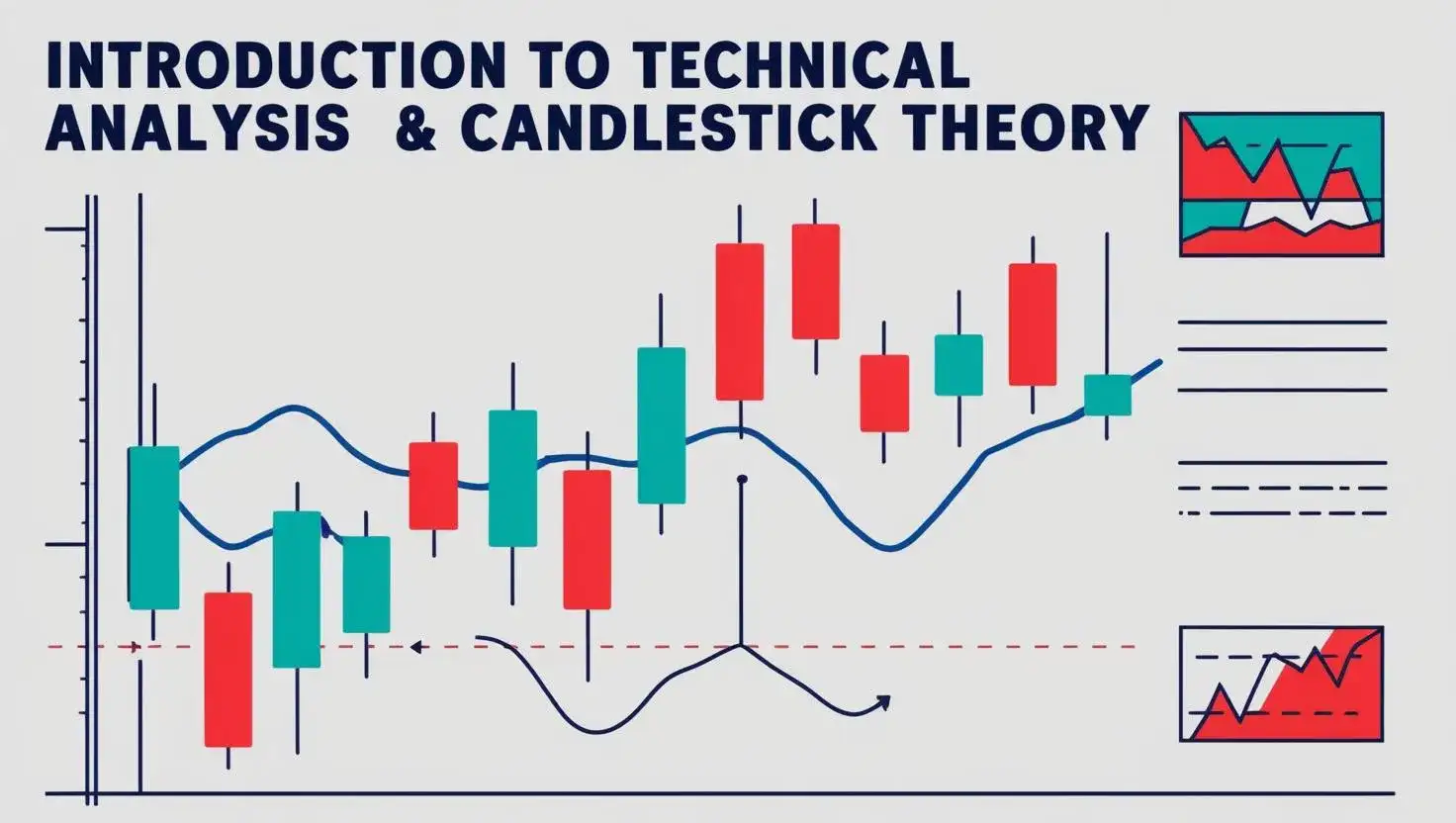

The introduction of technical analysis and candle principle

-

Money

The financial literacy ie the billionaire breaks the code

-

Digital marketing

Digital Marketing Masterclass by Neil Patel

-

Money

Technical Analysis Demistified-Full Guide to Trade

-

Productivity

Axel Required for Expert: Your Full Guide

-

Artificial intelligence

Business Professionals Batch 2 for A.I.

By the part of Mehra

Kalyan management has indicated that no pants-up demand from the recent moderation is likely to emerge in gold prices, as the marriage has not been postponed. Studed shares in 1qfy26 vs 30.4% in 1qfy25 remained stable at 30.2%. Stored income has increased by 30%.

Despite BASE support support and rising focus Sal Lisy (43% of India’s income), profitability positively surprised (EBITDA / PAT 35% / 49% YO), supported by procurement benefits and operating leverage leverage. Non-South now contributes> 50% of India revenue, studded shares ~ 30% and the Middle East mix improved. It maintains aggressive rollout guidance (fiscal year 26 – 90 welfare and 170 stores in 80 Kendre) and plans to launch regional brands during the year.

The ICCI Securities said, “Despite the elevated gold prices and the accelerating store rollout, with the continued trends of demand, we expect the welfare income to be strong. The ROCE is 21.8% and the net, with a net debt/equivalent of the GML, with the net.” Securities said.

Living events

Kalyan maintained its financial year 26 guidance 170 new showrooms (90 welfare + 80 Kendre), mostly by the Foko model.

“We mostly maintain our estimates, said ICICI, a modeling revenue / EBITDA / PT CAGR of 28% / 33% / 51% on FY 25-FY27E.

(Now you can subscribe to our Etmarkets WhatsApp channel)