Smartphone shipments grew by a minimum of 1% in the last quarter of 2025. Global shipments increased by 2% for the full year, according to preliminary data Counterpoint ResearchTo put a positive spin on it, it was the second consecutive year of growth,

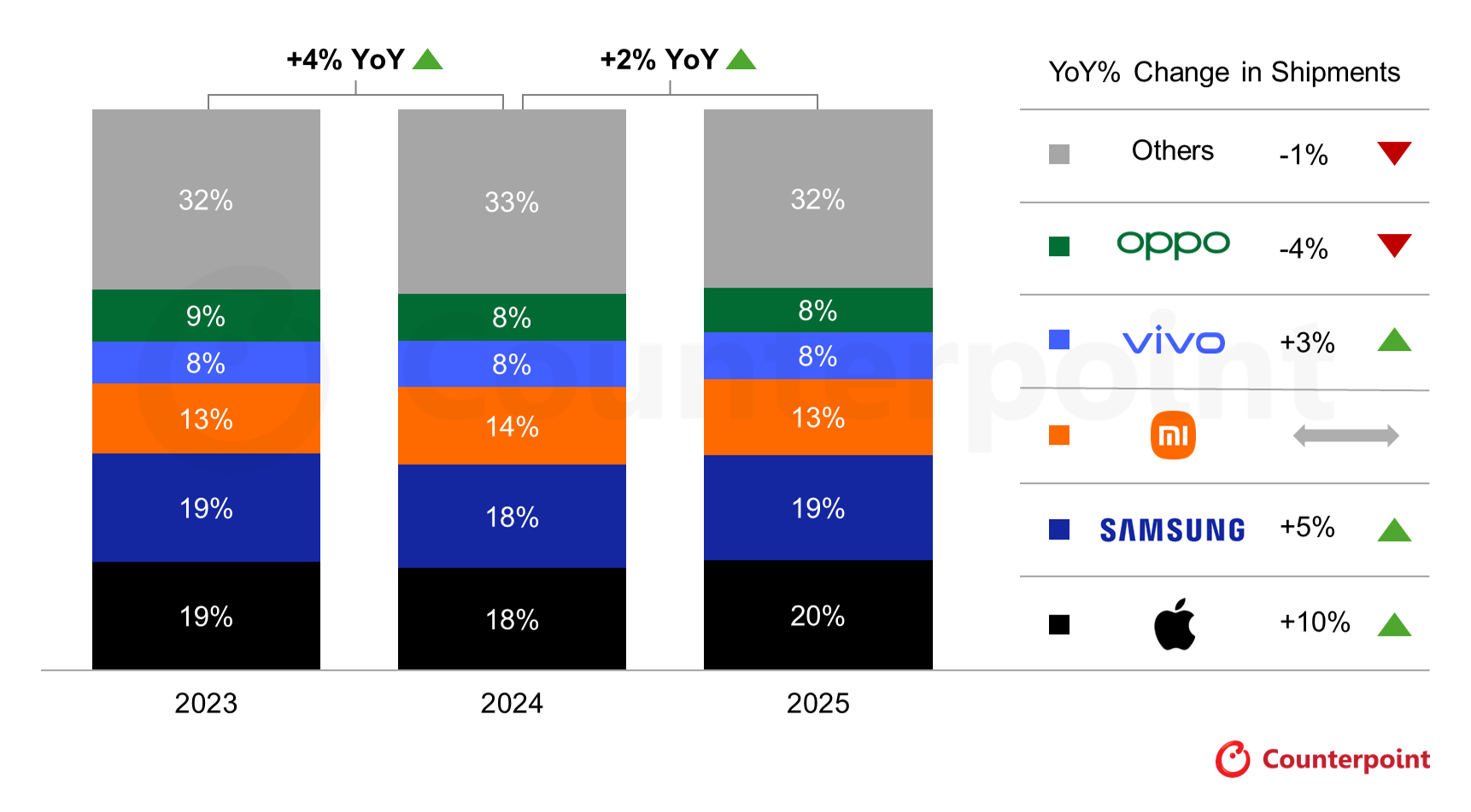

As expected, Apple became the largest smartphone maker globally with a 20% share – in other words, 1 in every 5 smartphones shipped in 2025 had the Apple logo on the back. In fact, Apple shipments grew the most (in the top 5) during the year, up 10% year-over-year.

The older iPhone 16 performed well in Japan, India, and Southeast Asia, while the new iPhone 17 series saw a surge in demand. One reason for the strong year of sales, competition This points to the COVID era, which shook up the upgrade cycle and left millions of users needing an upgrade in 2025.

Samsung had to settle for #2, but its 5% growth was solid compared to the rest of the top 5. The Galaxy S25 series along with the Galaxy Z Fold7 sold better than its predecessors, giving Samsung a boost in the premium segment. Meanwhile, rising demand for the Galaxy A-series gave Samsung a boost in the mid-range segment.

Xiaomi continued to maintain its third position with 13% market share. South America and Southeast Asia were major markets for the company.

Vivo rose 3% and swapped places with Oppo, which declined 4%. Analysts’ explanation for this swap is as follows – Vivo saw strong demand for its phones in India, while Oppo was facing tough competition in China and Asia-Pacific.

While they were outside the top 5, competition Nothing and Google were highlighted, with growth of 31% and 25% respectively during the full year 2025.

As far as what happens next, crazy memory prices could break the streak of annual increases. Research Director Tarun Pathak said, “The global smartphone market is set to soften in 2026 amid DRAM/NAND shortages and rising component costs, as chipmakers prioritize AI data centers over smartphones. Smartphone price increases are already beginning to surface. Against this backdrop, we have revised our forecast for 2026 down by 3% to shipment estimates.”